Why did nobody tell me investing was this easy?

The finance world has spent decades making this feel complicated. It isn’t. And once you see that, you cannot unsee it.

I was a physician who lived paycheque to paycheque and blamed my salary. I even had a financial advisor for two years and managed to save just over four thousand dollars before withdrawing it for something I can’t even remember now. The savings platform felt like someone else’s money. Distant, inaccessible, not really mine. And because I didn’t understand compounding, four thousand dollars felt laughably small. So I spent it.

That was the most expensive decision I ever made. Not because of what I spent. Because of what I walked away from.

Compounding in 1 Sentence.

Really, this isn’t hard.

Compounding is simply your money making money — and then that money making more money — until the whole thing starts to snowball beyond anything you initially put in. Done.

It’s not linear, it’s exponential, and the longer you leave it, the more unbelievably powerful it becomes. A thousand dollars invested at 20 earns far more than a thousand dollars invested at 40 — not because of what you put in, but because of how long it has to grow.

Time is the actual asset here. Not salary. Not a fancy portfolio. Just …time and patience.

The hard bit first, magic later:

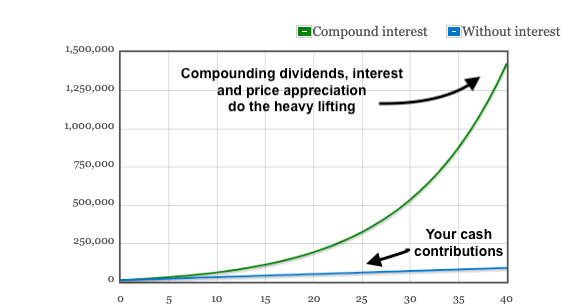

The painful truth is that in the early years, it barely feels like anything is happening. It’s disheartening. You’re putting money away every month, and the growth feels almost pointless. This is the stage I previously gave up, as so many do. But this is exactly where the graph is building its runway.

Compounding is exponential, not linear.

The rise comes later, and when it does, it’s steep. Stay in long enough and the curve does something that feels shocking. The women who build real wealth aren’t the ones who earn the most. They’re simply the ones who didn’t quit early.

Growth that smashes your savings account. Think closer to 10%.

Global index ETFs (Exchange Traded Funds) are funds that simply track the entire world’s stock market. No stock picking, no wealth manager, no suit. Just the whole market, in one diversified easy fund. They have historically returned around 10% annually over the long term. Not every year, and yep, some years are pretty brutal, but averaged out over decades, that number holds remarkably well. A damn sight better than the 2.5% savings account from your bank that feels safe but is a total waste of your years in the market.

Why your wealth manager doesn’t want you to know this.

You’re likely paying their 1% advisory fee plus another 0.9% in hidden fund management costs. That’s nearly 2% annually quietly draining your returns — on a portfolio that, statistically, will still underperform a cheap index fund you could buy yourself in TEN minutes.

Eugene Fama won the Nobel Prize in Economics for proving that markets price in information so efficiently that active managers cannot consistently exploit it. His conclusion after a career of research: approximately 97% of actively managed funds show no skill sufficient to justify their fees. A Nobel laureate said this. The finance industry just hoped you wouldn’t hear about it.

So let’s put it all together.

10% average annual ETF returns + compounding.

This is where the projections become almost shocking. Plug your own numbers into a compounding calculator and prepare to feel something shift.

I’ll go deep on exactly which funds, why I chose them, and how to actually buy them in the next article. But for now, just sit with this: it isn’t complicated. It never was.

Having some fun with it

One of the things that kept me going in the early years, when the growth felt invisible, was being able to model my own investments. To plug in my numbers and actually see what the curve looked like at year 10, year 20… year 30.

Seeing it visually, with your actual figures, changed something in my brain.

It stops feeling abstract and starts feeling frankly inevitable. In a future piece, I am going to show you exactly how to use AI to build your own investment model, no spreadsheet experience needed, because I genuinely believe it is one of the most motivating things you can do for yourself. I’d love for you to subscribe so I can share my learning with you.